What changed. Nothing else.

Strise watches the network behind your customer, not just the name. What changed reaches your analyst. What didn't, closes automatically.

Sound familiar?

Annual reminders fire on the same date regardless of what's changed. High-risk entities and no-change entities go through exactly the same review process.

Entities with no material changes still hit the full review queue, consuming the same analyst hours as genuinely complex and high-risk cases.

Calendar-based monitoring leaves material changes undetected for months at a time. Real risk stays invisible until the next scheduled review date arrives.

Review volumes don't grow linearly, they spike. One team, one year, and suddenly the numbers don't work no matter how hard your analysts push.

Two back-books, both past recommended review timelines. And the next periodic review cycle is already queuing up behind the one that's still running.

The change happened in the ownership chain, not on the customer's record. Your tool screened the name. The risk slipped through every check.

The difference Strise makes.

What customers say.

The review that prepares itself.

Onboarded. Monitoring live

Every onboarded entity enters continuous monitoring from day one. Risk tier sets the frequency.

All signals. Always on

The whole network around your customer, watched continuously. Ownership, sanctions, directors, PEPs, nothing missed.

Nothing changed. Closes

Entities with no material changes confirmed and closed automatically. Audit log built.

Change detected.

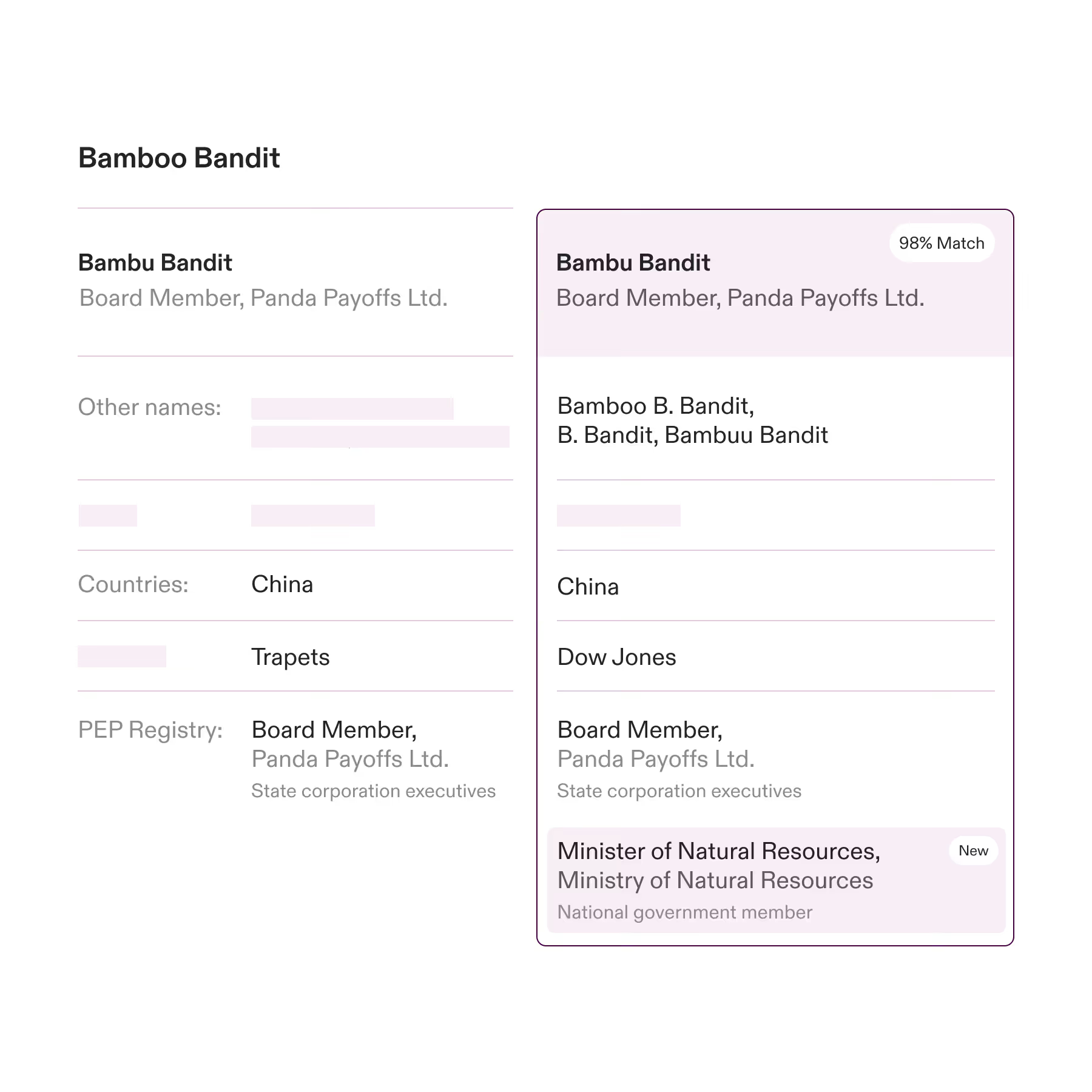

Your analyst gets a complete case file, the change documented, evidence cited, context provided.

Automate Ongoing Due Diligence.

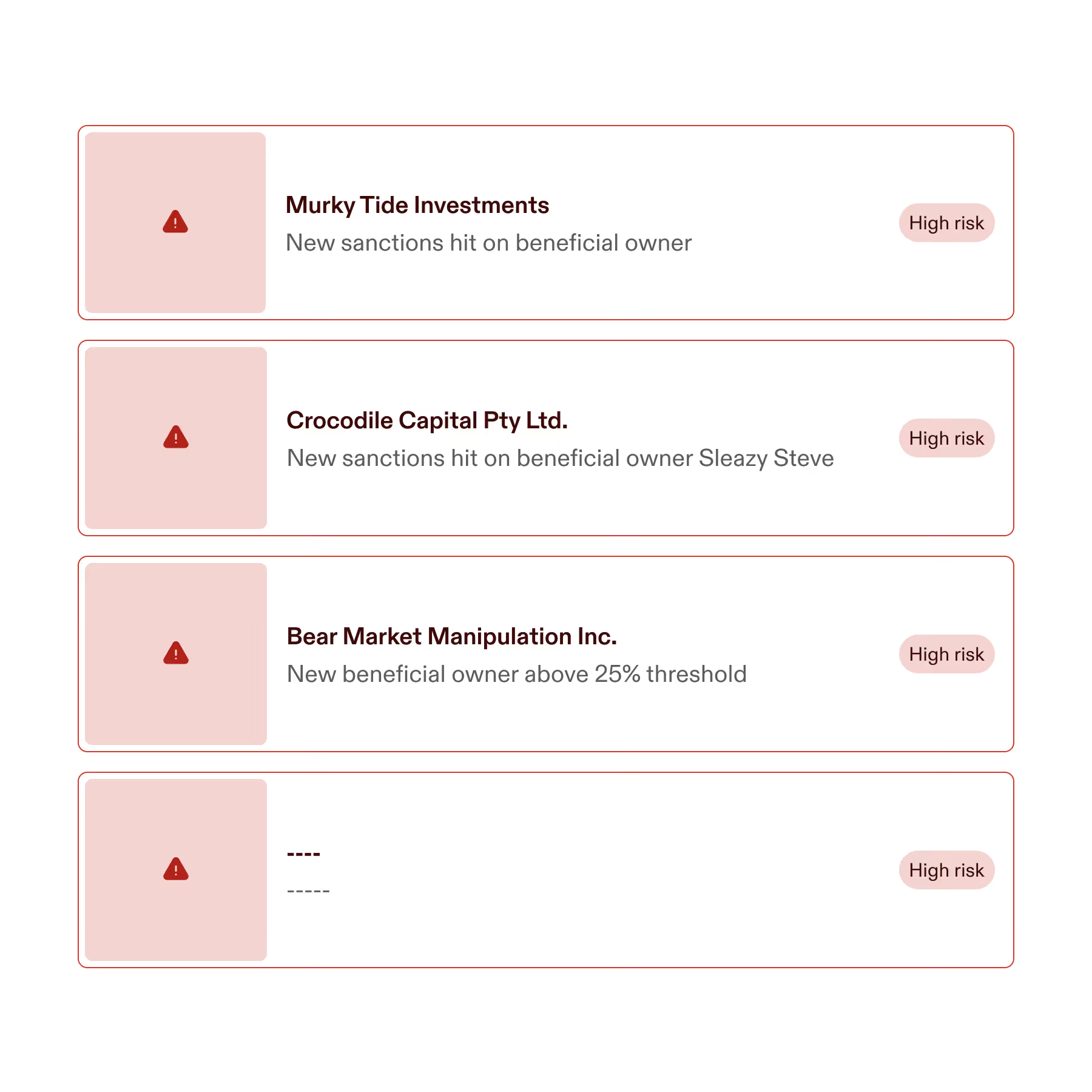

Know the moment something changes. Not the month after.

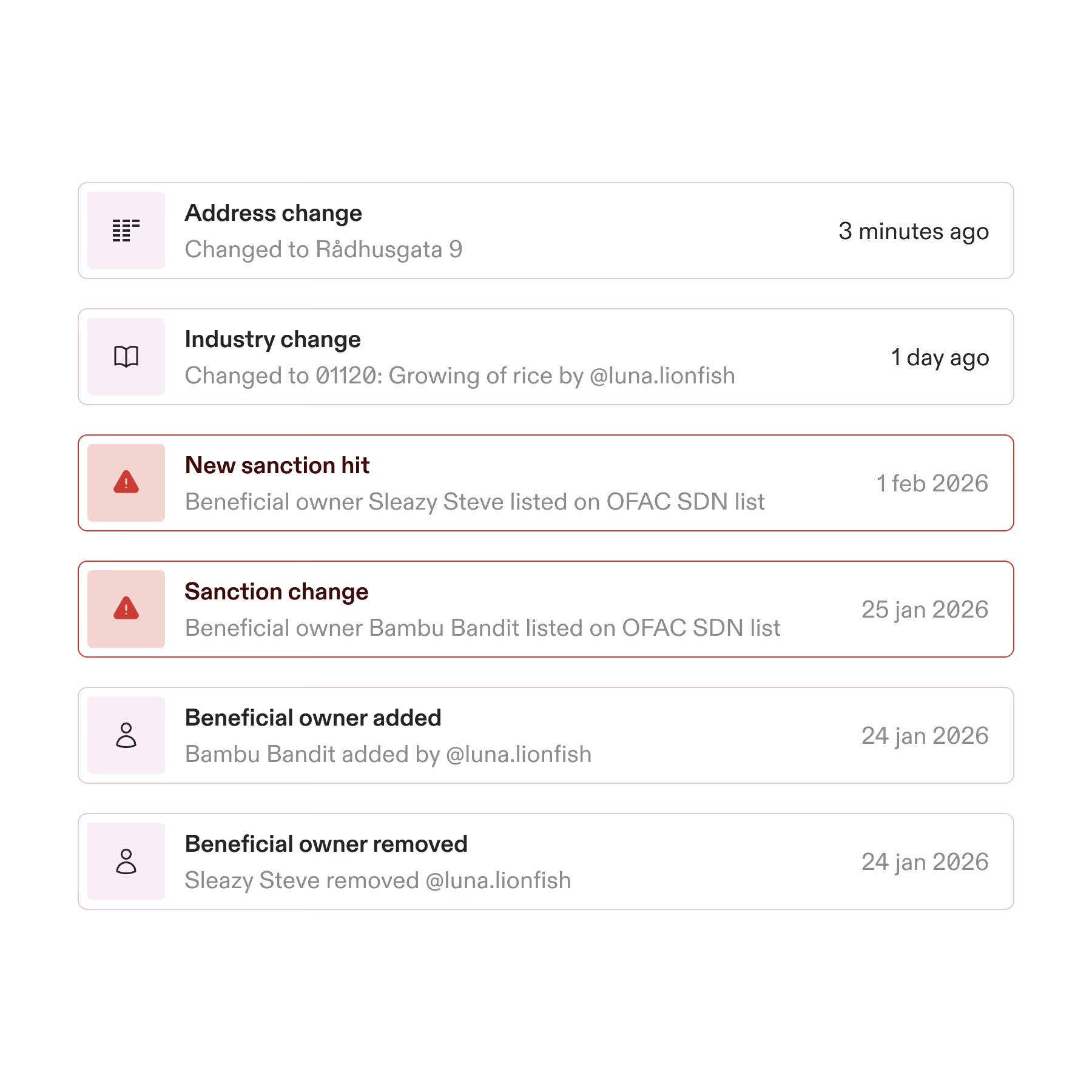

Your alert feed surfaces director changes, sanctions hits, and adverse media as they happen. You know immediately — not at the next scheduled review date.

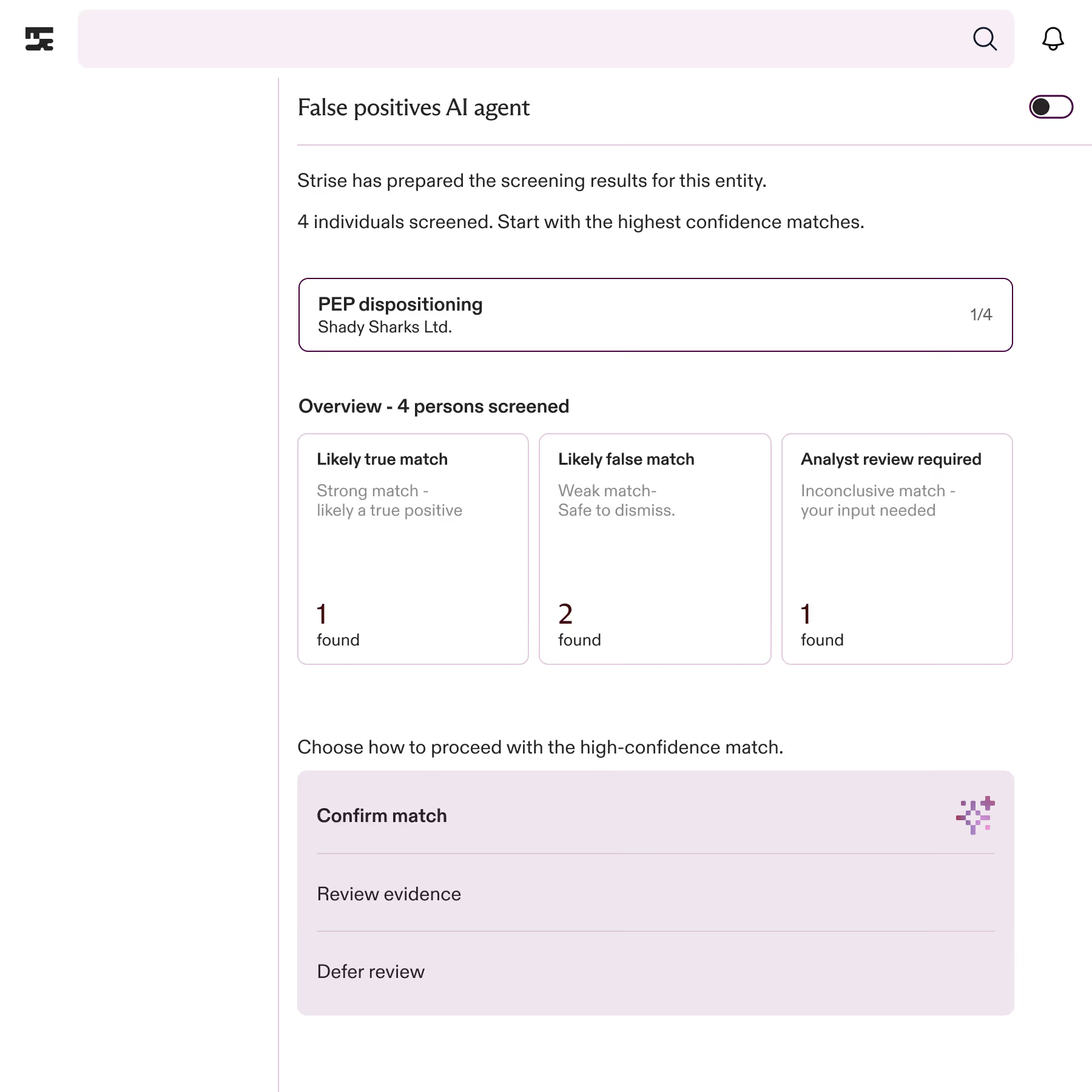

Alerts triaged. Only real matches reach your analyst.

For every PEP, sanctions, and adverse media alert, AI assesses match confidence and separates likely hits from false positives. Analysts confirm, dismiss, or escalate, instead of investigating from scratch.

Every alert documented. Context attached. Regulator-ready.

Each alert includes what changed, the compliance implications, and the recommended next action. Every check, every closure, every analyst decision logged with source, timestamp, and rationale.

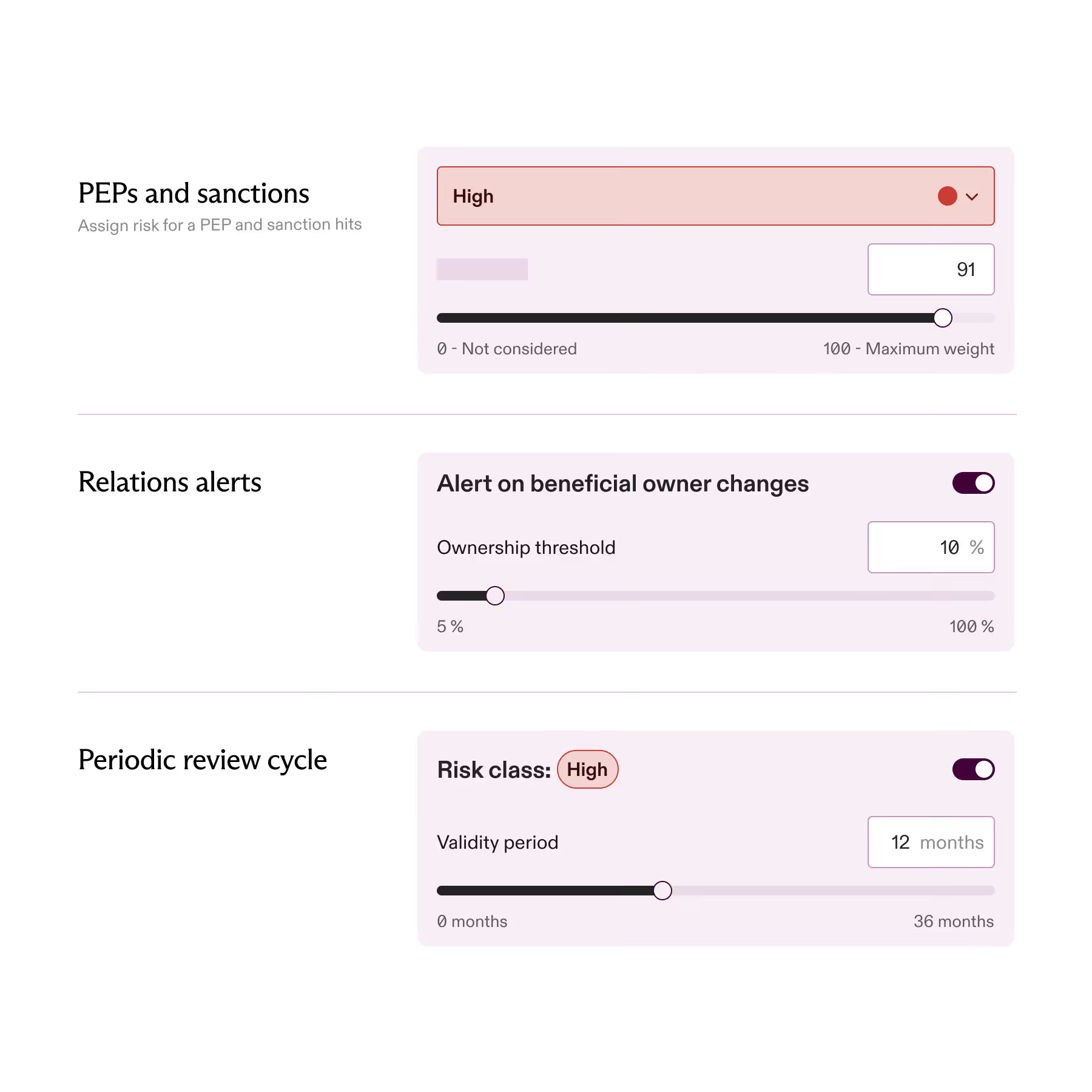

Your risk rules set the thresholds. Not the system.

Set what triggers a review and what resolves without one. Different rules for different risk tiers, configured by your team, not locked in by default. You own the policy. Strise enforces it.

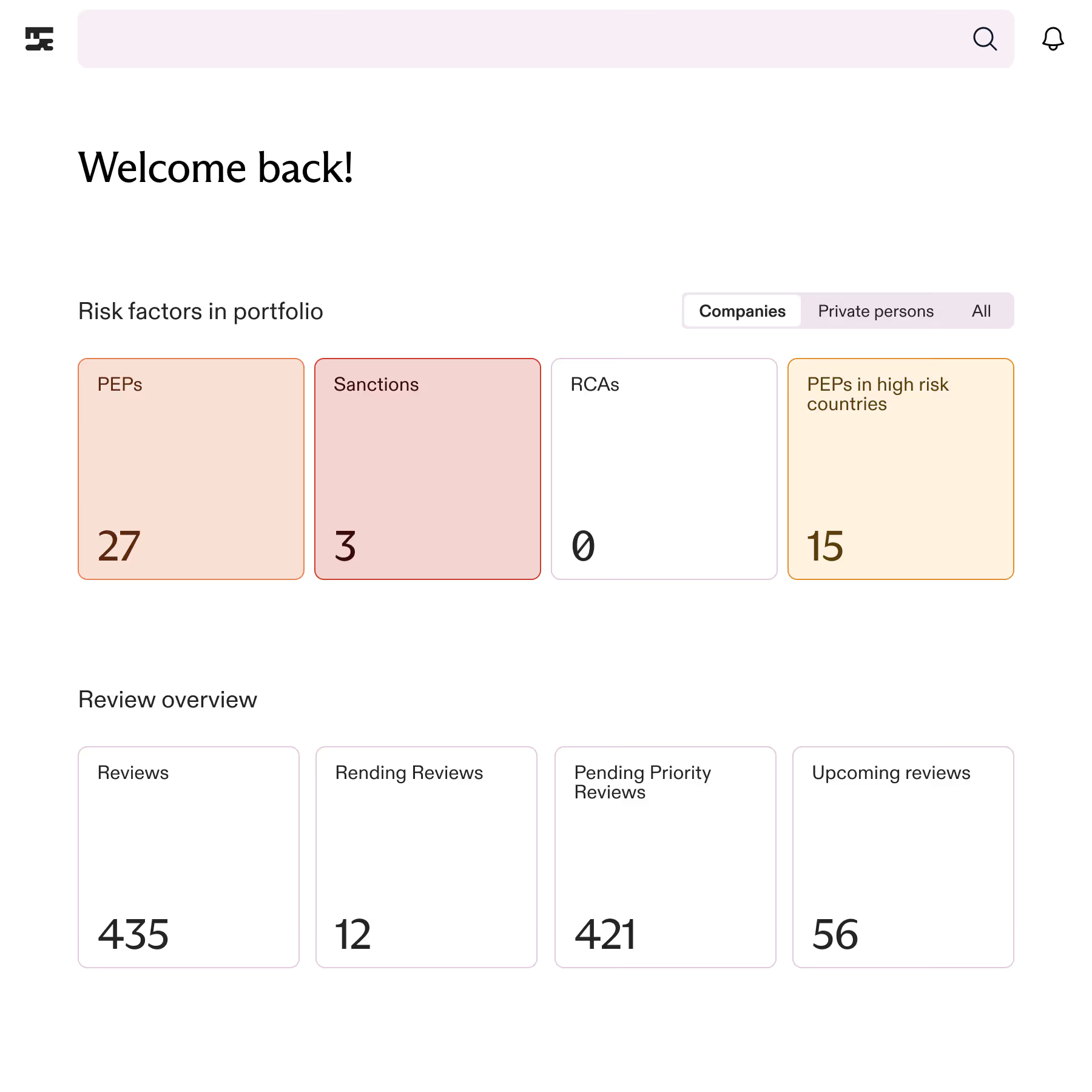

Your entire portfolio. Risk-ranked. At a glance.

Sorted by current risk level, open alerts, and upcoming review dates, all visible at once. The entities that need attention rise to the top. Everything else stays out of your way.

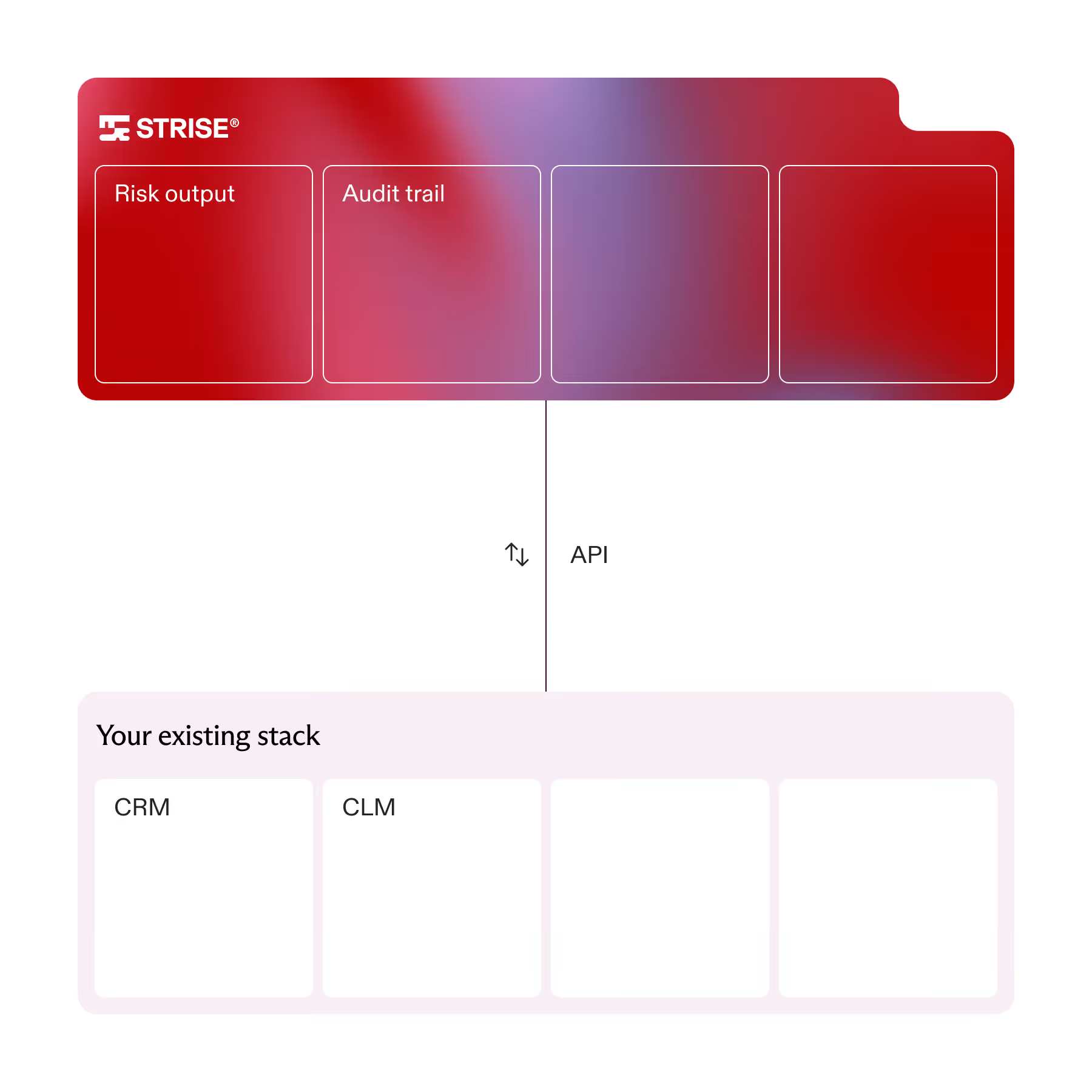

Connects to your CRM, TMS, and CLM from day one.

Push alerts and review outcomes into the tools your team already uses. Strise fits into your workflow, it doesn't ask your team to change theirs.

Every decision recorded. Regulator-ready.

Every check, every closure, every analyst decision, logged with source, timestamp, and rationale. Your audit trail is complete before anyone asks for it.

Things we get asked. Answered.

Sanctions and PEP lists are checked daily, overnight, results surface the next morning. Registry changes vary by jurisdiction, but we check as soon as registries publish updates. You're not waiting a week to find out something changed.

Any material change: a new director, an ownership transfer, a sanctions update, a PEP designation, or a significant adverse media hit. Low-noise changes that don't affect risk don't trigger anything, your team isn't flooded with non-events.

Matching uses multiple data points together — name, date of birth, nationality, jurisdiction, entity type. When they don't line up, it's flagged as a likely false positive automatically. Your team reviews what's genuinely ambiguous, not everything that shares a name.

Yes — that's the point. Entities with no material changes are automatically confirmed and closed, with a full audit record. Your analysts spend time on cases that need a human, not on signing off that nothing happened.

Dow Jones for PEP and sanctions lists. Global registry connections for director and ownership changes. Global news sources for adverse media. All checked together so you get context, not just a raw hit that tells you nothing on its own.

Yes. The portfolio dashboard shows risk tiers, upcoming and overdue reviews, PEP and sanctions exposure, and recent changes, across your full book. One screen. No manual reporting required to understand where you stand.

Every check, every alert, every decision, logged automatically with timestamp, user, source, and rationale. When a regulator asks how you run ongoing due diligence, you pull the trail and show them. No scrambling, no reconstructing from emails.

Both. You set a review cadence per risk tier — annual for low, six-monthly for high, whatever your policy requires. Event-triggered reviews fire on top of that when something material changes. You get scheduled coverage and real-time response.